Inflation : implications pour l'immobilier

Immobilier et inflation : principales observations

Cet article, basé sur les données de décembre 2021 de Savills World Research, reprend les observations clés concernant l'immobilier et l'inflation, soulignant la nuance de leur relation.

L'immobilier est souvent perçu comme un rempart contre l'inflation, mais la réalité est plus complexe. Toutes les propriétés ne réagissent pas de la même manière aux pressions inflationnistes, et comprendre les nuances est crucial dans le climat économique actuel.

L'inflation : transitoire ou profonde ?

Définie comme un phénomène de courte durée, l'inflation est devenue un point central de discussion parmi les décideurs politiques. Le débat se concentre sur la question de savoir si l'inflation est effectivement transitoire ou si elle a des racines plus profondes. Des éléments tels que l'ampleur des mesures de relance monétaire et fiscale post-COVID-19 ainsi que les données salariales alimentent la discussion.

Impact sur l'immobilier

Bien que l'immobilier serve traditionnellement de protection contre l'inflation, des preuves récentes suggèrent une image plus nuancée. La croissance économique, l'inflation par la demande et l'inflation par les coûts impactent différemment l'immobilier. Les propriétaires encourent un risque accru dans des environnements dominés par l'inflation par les coûts, ce qui entraîne une croissance économique plus lente et une demande réduite.

Stratégies d'investissement

Malgré les défis rencontrés, l'immobilier demeure une option attrayante pour les investisseurs en quête de protection contre l'inflation. Les actions ont tendance à bien se comporter lors de périodes de hausse des prix, tandis que les produits à revenu fixe font face à des défis en raison de la diminution du pouvoir d'achat.

Facteurs géographiques et sectoriels

Les différences géographiques et sectorielles jouent un rôle significatif dans la manière dont les actifs immobiliers réagissent à l'inflation. Des facteurs tels que les termes des contrats de location et les caractéristiques propres à chaque marché régional varient, affectant ainsi le degré de protection offert contre l'inflation.

Conclusion

Bien que l'immobilier puisse aider à atténuer les risques liés à l'inflation, les investisseurs doivent tenir compte des nuances sectorielles et géographiques pour maximiser les rendements. Comprendre l'interaction entre l'immobilier et l'inflation est crucial pour naviguer dans le paysage économique complexe d'aujourd'hui.

Vous souhaitez en savoir plus ? Découvrez l'article complet "Inflation: Implications for Real Estate" (anglais)

Source : December 2021, Savills World Research - The relationship between real estate and inflation is more nuanced than conventional wisdom suggests - Oliver Salmon

Articles liés

Un événement exceptionnel au fil de l’eau avec Luxury Places

Le 21 septembre dernier, Luxury Places a organisé un événement exclusif dans une incroyable propriété pieds dans l'eau à Perroy, offrant à ses invités une journée inoubliable, sublimée par un cadre exceptionnel et un temps magnifique. Sous un ciel bleu et ensoleillé, nos partenaires de prestige ont enrichi cette expérience, combinant convivialité, découverte et échanges.

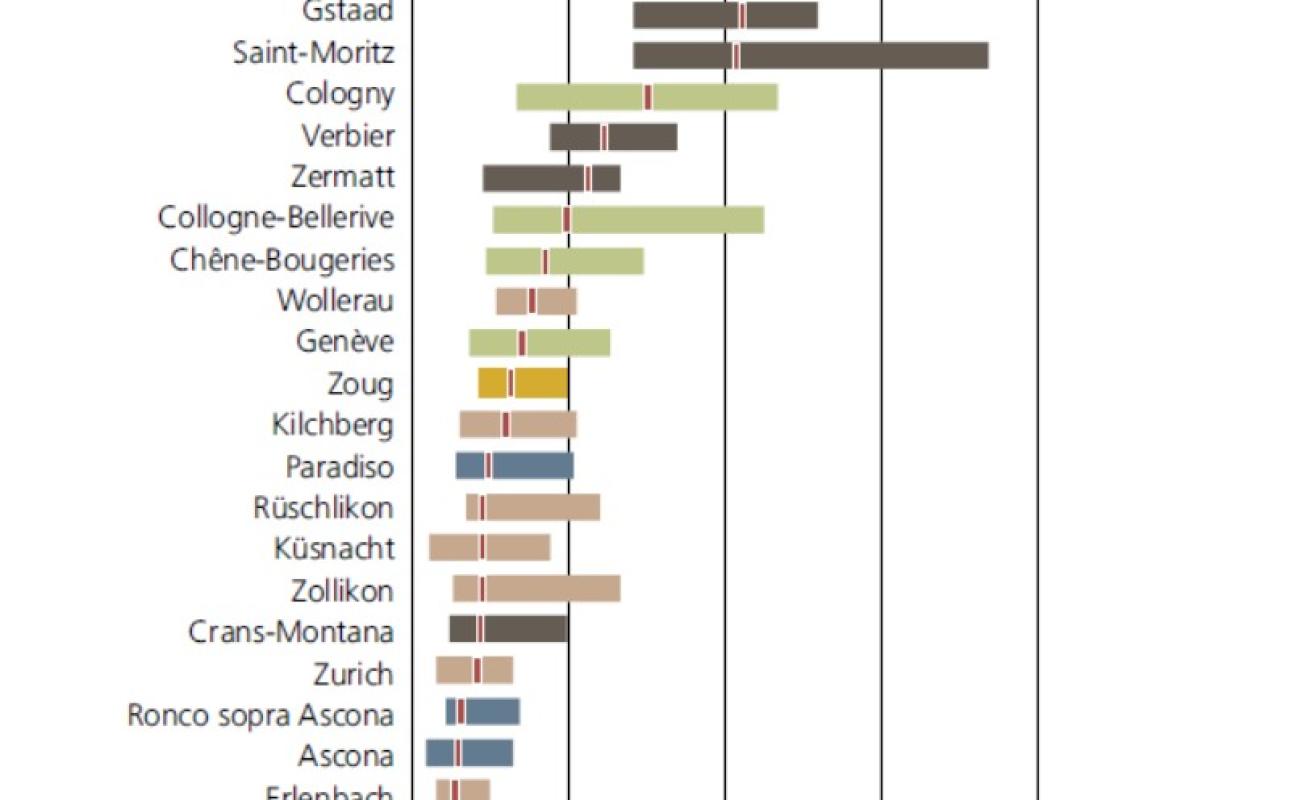

UBS Swiss Real Estate Bubble Index 2e trim. 2018

D’après la dernière version du rapport édité par UBS, le marché immobilier Suisse s’éloigne encore un peu plus d’une situation de bulle.

Quelques faits intéressants :